In 1996 Peyman Milanfar, a reader of Mathematics Magazine, presented a quick way to estimate monthly payments on a loan, passed down from his grandfather, who had been a merchant in 19-century Iran:

The interest is calculated as

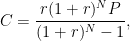

The exact formula given in finance textbooks is

where C is the monthly payment, r is the monthly interest rate (1/12 the annual interest rate), N is the total number of months, and P is the principal. Rendered in that notation, the folk formula becomes

“In many cases, Cf is a surprisingly good approximation to C,” particularly when the principal is fixed, the monthly interest rate is sufficiently low, and the total number of months is sufficiently high, Milanfar writes. For example, for a four-year loan of $10,000 at an annual rate of 7% compounded monthly, the precise formula gives a monthly payment of $239.46, while the folk formula gives $237.50.

“While its origins remain a mystery, the method is still in use among merchants all around Iran, and perhaps elsewhere.”

(Peyman Milanfar, “A Persian Folk Method of Figuring Interest,” Mathematics Magazine 69:5 [1996], 376.)